Get Ready for the Bargain Bin Market: Jobs & Housing Numbers Coming

Wemimo Abbey of Esusu, Sasan Goodarzi of Intuit

Three questions dominate my thinking about the markets and the economy these days:

Is the consumer strong or just spending?

Should investors be shifting into fixed income and thinking about tax equivalent yield?

What are the characteristics of companies creating sustainable advantages now?

The last few days have brought interesting answers, many of which I’ve gotten from CEOs operating in this volatile environment.

The framing of the first question came to me during a Friday conversation on CNBC with RockCreek CEO Afsaneh Beschloss (video below). I keep hearing all this talk about how the consumer remains strong because the consumer is still spending. But those aren’t necessarily the same things.

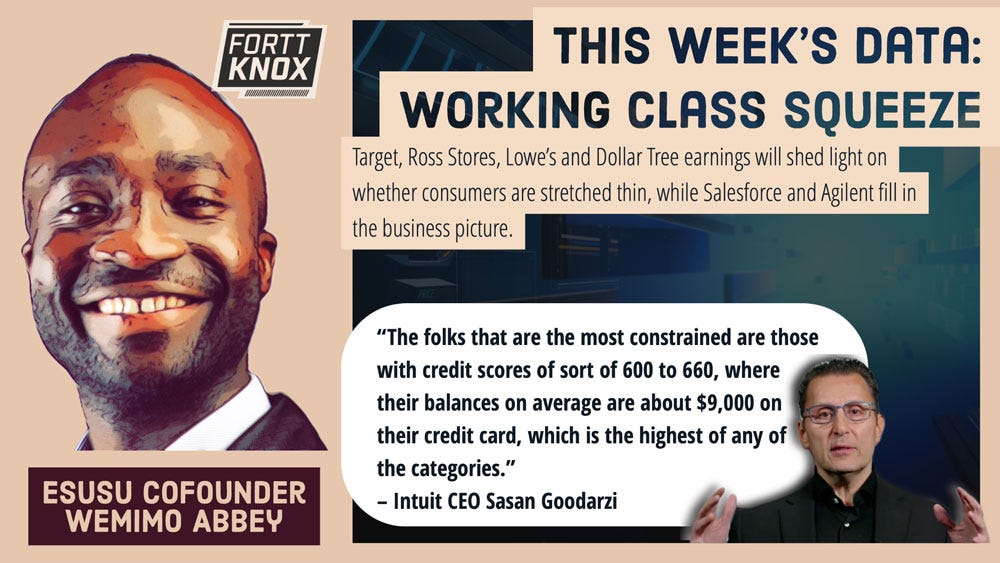

Two other conversations this week drove that home. I spoke with Intuit CEO Sasan Goodarzi after his earnings report (video below), and he noted a trend his Credit Karma unit is seeing: Consumers with subprime and near-prime credit scores are having a harder time getting access to capital. That means while those consumers are spending money, they’re racking up expensive debt in the process, and lenders are less eager to keep the money flowing. I also spoke with Esusu cofounder Wemimo Abbey (video below). He said renter debt-to-equity ratios have spiked into a dangerous area.

That lines up with what we heard from Walmart, Home Depot and TJX earnings reports. Walmart said inflation-pressured consumers are buying affordable groceries and have less to spend on discretionary items. That seemed to be part of the reason why do-it-yourself spending was down at Home Depot, and why TJX’s HomeGoods store sales slumped 7%. Yes, the consumer’s spending. But showing more strength, or strain?

The second question has to do with the tension between stocks on one side, and investments like bonds and certificates of deposit (CDs) on the other.

As interest rates rise, it prompts a shift in investor behavior. Higher interest rates mean you don’t have to take as much risk to get a return of close to 5% on your money. And that makes it harder to argue that investors should just buy stocks. Even more intriguing, people in a high tax bracket might consider investing in municipal bonds — debt offered by towns, cities and states. The income from those bonds is generally exempt from federal taxes. So a 5% yield on a muni bond is equivalent to an 8.7% yield if you’re in the highest tax bracket. (Click here to calculate tax equivalent yields.) I’m an anchor on a financial network, so I’ve gotta talk about that.

And finally, differentiation. Beyond the short-term stock moves, what separates the companies that are going to thrive from the ones that are just casting about? Two of the CEOs I spoke with over the last few days had challenging cross currents to explain.

Medtronic CEO Geoff Martha is trying to improve profit margins while turning around a troubled U.S. diabetes business, and while short-staffed hospitals are still finding it difficult to get elective procedures done using Medtronic’s technology. He told me about the progress he’s making (video below).

Autodesk CEO Andrew Anagnost is shifting his company to a different billing cycle for multi-year deals, and that’s caused some customers to spend early ahead of that change and will temporarily dry up some cash flow during the transition (video below). It’s one of those things that can freak investors out in the short term — the stock closed down about 13% on Friday — but if it works out the way Autodesk envisions, it could bring benefits to the company.

Coming this week, more data to fill in whether we’re seeing a strained working class consumer — spending, but maybe not so strong. The guidance from Target, Ross Stores, Lowe’s and Dollar Tree will warrant especially close attention. And then we’ll get some big-picture data on the U.S. economy, including non-farm productivity, initial jobless claims, pending home sales and mortgage applications.

As long as employment stays relatively strong, consumers with stretched credit probably can keep spending. And as long as consumers keep spending, businesses can probably keep employing people. Another question is, as interest rates rise and credit gets both more expensive and harder to come by, does that virtuous loop come undone?

Esusu Cofounder Wemimo Abbey on Working Class Economic Hardship: CNBC Working Lunch

Medtronic CEO Geoff Martha on Turnaround Progress

ThoughtSpot CEO Sudheesh Nair on Moving Beyond Dashboards in Analytics

Intuit CEO Sasan Goodarzi on Small Business Resilience and Consumer Strain

Autodesk CEO Andrew Anagnost on the Billings Shift, Cash Flow, and Macro Impact

RockCreek CEO Afsaneh Beschloss on the Market (Finally) Believing the Fed

ServiceNow CEO Bill McDermott on How Enterprise Software Sales is Changing